Mortgage Investment Corporation Things To Know Before You Buy

Mortgage Investment Corporation Things To Know Before You Buy

Blog Article

The Mortgage Investment Corporation PDFs

Table of ContentsSome Ideas on Mortgage Investment Corporation You Need To KnowMortgage Investment Corporation Fundamentals ExplainedRumored Buzz on Mortgage Investment CorporationThe 4-Minute Rule for Mortgage Investment Corporation10 Simple Techniques For Mortgage Investment CorporationExcitement About Mortgage Investment Corporation

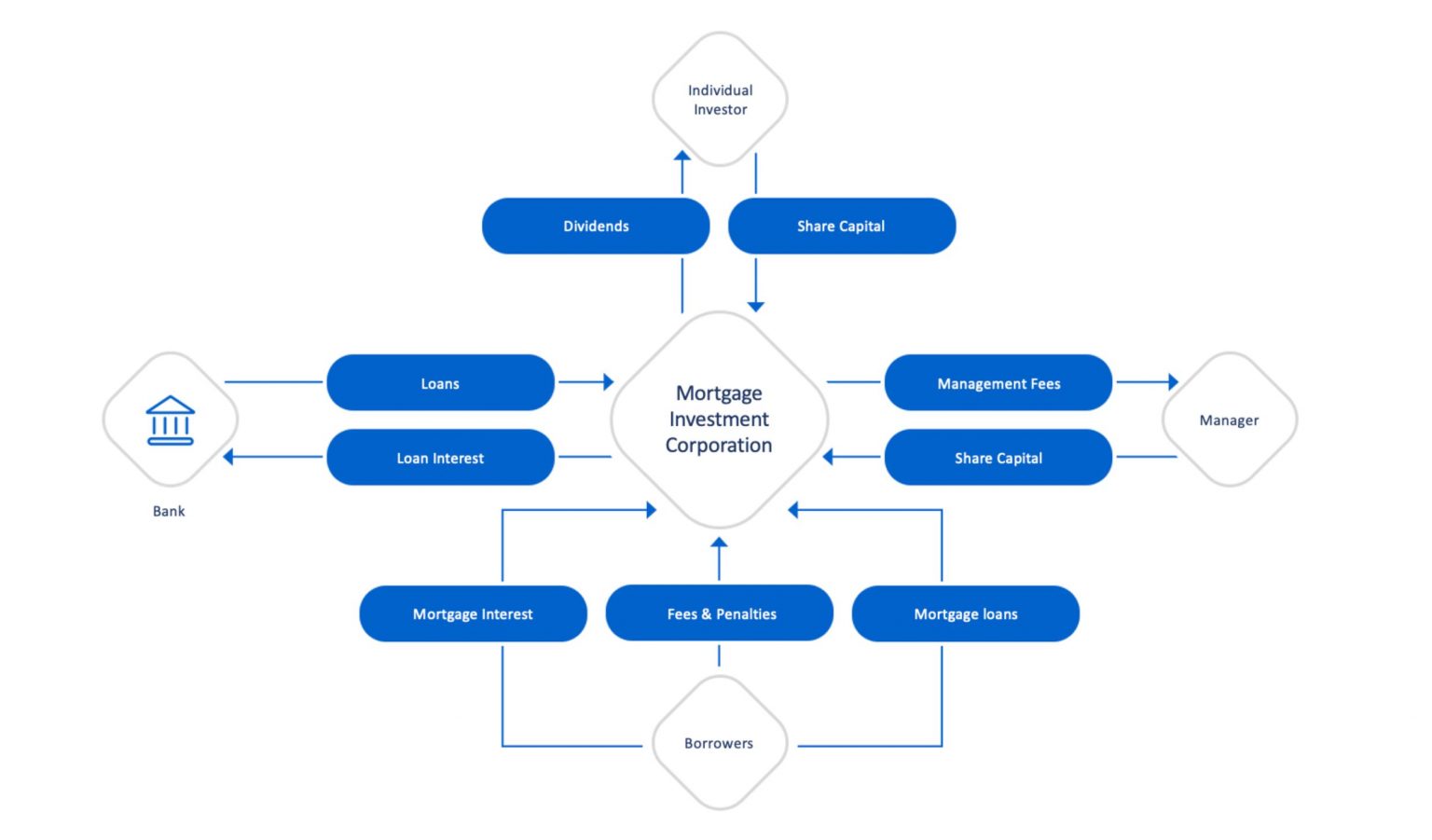

And due to the higher threat profile of these debtors, they can be billed a greater passion price. Today in 2014 most standard home loan prices are around 3% (Mortgage Investment Corporation). However home loan rates from a MIC is generally around 9% to 12% Tolerable eh? Management charges and various other expenses connected with running the MIC eat away about 2% to 4% of the overall earnings, so before tax obligation, depending upon the mix of home loans

Getting The Mortgage Investment Corporation To Work

What is the mix between 1st and 2nd home mortgages? What is the size of the MIC fund? This info can be located in the offering memorandum which is the MIC matching of a shared fund program.

Some MICs have limitations on the withdrawal procedure. The MIC I have picked is Antrim Investments.

and largely concentrate on household home mortgages and little business lendings. Right here's a check out Antrim's historical returns. I seem like the property allotment, expected returns, and diversity of genuine estate for this MIC match my threat tolerance and investment requirements to ensure that's why I picked this set. Over the last 3 years the annual return has actually been 7.17% to financiers, so I will assume as the anticipated return on my new $10,000 MIC investment for the time being.

The 7-Minute Rule for Mortgage Investment Corporation

To open an account with Canadian Western we just load out an application kind which can be discovered on its internet site. Next we give directions to our trustee to get shares of the MIC we desire.

We'll likewise require to send by mail a cheque to the trustee which will represent our initial down payment. About 2 weeks later we must see cash in our new trust account There is a yearly fee to hold a TFSA account with Canadian Western, and a $100 purchase fee to make any buy or offer orders.

MICs aren't all that and a bag of potato chips There are genuine threats as well. Many MICs keep a margin of security by you could try here maintaining a reasonable lending to value proportion.

3 Simple Techniques For Mortgage Investment Corporation

This time, publicly traded ones on the Toronto Supply Exchange. / edit]

This constant circulation of money makes sure that lenders constantly have funds to provide, offering even more people the opportunity to attain homeownership. Capitalist standards can additionally make sure the stability of the home check this loan industry.

After the loan provider markets the finance to a home mortgage capitalist, the loan provider can use the funds it receives to make even more lendings. Mortgage Investment Corporation. Supplying the funds for lending institutions to produce more finances, financiers are essential since they set standards that play a role in what kinds of fundings you can get.

Not known Factual Statements About Mortgage Investment Corporation

As home owners repay their home loans, the settlements are gathered and distributed to the personal financiers that bought the mortgage-backed protections. Unlike federal government firms, Fannie Mae and Freddie Mac do not guarantee car loans. This suggests the exclusive financiers aren't ensured compensation if debtors don't make their finance repayments. Because the investors aren't protected, adjusting lendings have more stringent standards for establishing whether a consumer certifies or not.

Financiers likewise handle them differently. Instead, they're marketed directly from lenders to exclusive investors, without entailing a government-sponsored business.

These firms will package the fundings and market them to exclusive capitalists on the second market. After you shut the finance, your lender may offer your loan to a capitalist, yet this usually does not change anything for you. You would still pay to the lender, or to the mortgage servicer that manages your home mortgage settlements.

After the lending institution markets the lending to a home mortgage investor, the loan provider can make use of the funds it gets to make more finances. Besides giving the funds for loan providers to produce even more loans, financiers are essential due to the fact that they set standards that play a duty in what kinds of financings you can obtain.

3 Simple Techniques For Mortgage Investment Corporation

As home owners pay off their home loans, the payments are gathered and dispersed to the private financiers that bought the mortgage-backed safety and securities. Unlike government companies, Fannie Mae and Freddie Mac don't guarantee lendings. This means the exclusive investors aren't guaranteed payment if borrowers do not make their loan settlements. Considering that the capitalists aren't secured, conforming fundings have stricter guidelines for figuring out whether a customer certifies or not.

Division of Veterans Matters establishes standards for VA financings. The United State Department of Agriculture (USDA) sets guidelines for USDA fundings. The Government National Mortgage Association, or Ginnie Mae, supervises government home financing programs and guarantees government-backed car loans, protecting exclusive capitalists in situation debtors default on click now their financings. Jumbo loans are home loans that exceed adapting loan limits. Since there is even more threat with a bigger mortgage quantity, big fundings tend to have more stringent customer eligibility needs. Financiers also handle them differently. Conventional jumbo fundings are normally as well large to be backed by Fannie Mae or Freddie Mac. Rather, they're marketed straight from loan providers to exclusive investors, without involving a government-sponsored business.

These companies will package the car loans and offer them to personal investors on the second market. After you shut the lending, your loan provider may sell your loan to an investor, but this typically does not change anything for you. You would still pay to the loan provider, or to the home loan servicer that manages your home loan settlements.

Report this page